I’ve been neck-deep in the AI software market since 2021, and honestly? 2025 feels different from anything I’ve seen before. We’re past the initial “ChatGPT changed everything” shock, and now we’re watching something more interesting unfold—the market is maturing, consolidating, and frankly, getting a lot more practical.

Last month, I sat through three different vendor pitches where companies claimed their AI would “revolutionize everything.” But here’s what I’ve learned from actually implementing these tools with real clients: the AI software market trends in 2025 aren’t about revolution anymore. They’re about evolution, integration, and figuring out what actually works when the rubber meets the road.

In this article, I’m breaking down the real trends shaping the AI software market right now—not the buzzwords from press releases, but what I’m seeing in actual budgets, actual implementations, and actual results. Whether you’re trying to decide where to invest, which tools to adopt, or just trying to make sense of this rapidly shifting landscape, I’ll give you the practical insights I wish someone had shared with me two years ago.

The Great Consolidation: Fewer Players, Bigger Platforms

Here’s something that caught me off guard in early 2025: the number of standalone AI tools is actually decreasing. I know that sounds counterintuitive when you hear about new AI startups launching every week, but stay with me.

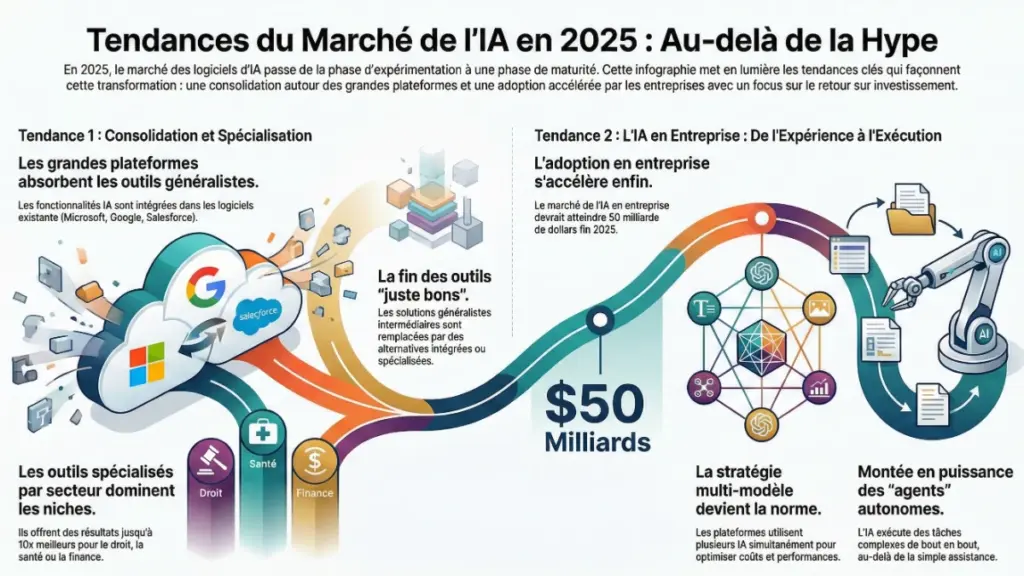

What’s happening is a massive consolidation wave. Remember when we had separate tools for AI writing, AI image generation, AI coding, and AI analytics? Those walls are crumbling fast. The major platforms—think Microsoft, Google, Salesforce, Adobe—are aggressively integrating AI capabilities directly into their existing software suites.

Just last quarter, I watched three of my clients cancel their standalone AI writing tool subscriptions (combined cost: around $4,500 annually) because Microsoft 365 Copilot now handles 80% of what they needed. That’s not a unique story. According to Gartner’s latest research, integrated AI features in existing enterprise software are capturing market share from point solutions at an accelerating rate.

What this means practically:

- For large enterprises: You’re likely getting AI capabilities bundled into software you already pay for. Before buying another AI tool, audit what’s already included in your Microsoft, Google, or Salesforce licenses.

- For standalone AI vendors: Differentiation is everything. The survivors are going deep on specific use cases (like legal document review or medical diagnostics) rather than trying to be general-purpose.

- For buyers: The math is shifting. A $20/month standalone tool needs to deliver serious value to justify its existence when your existing software includes “good enough” AI features.

The countertrend worth watching: specialized AI tools that do one thing exceptionally well are still thriving. I’m seeing companies pay premium prices for best-in-class solutions in areas like code review, customer service automation, or financial forecasting. The middle ground—tools that are “pretty good” at general tasks—is getting squeezed out.

Multi-Model Strategy Becomes Standard Practice

Remember when choosing an AI tool meant choosing between GPT-4, Claude, or Gemini? That binary decision is basically over in 2025.

Every sophisticated AI platform I’ve evaluated this year uses multiple models simultaneously. It’s called “model routing” or “model orchestration,” and it’s becoming table stakes. Here’s how it works in practice: the system analyzes your request and routes it to whichever AI model handles that specific task best—and often combines outputs from multiple models.

I saw this firsthand when testing a new content platform last month. Simple social media posts went to a fast, cheap model (keeping costs down). Complex long-form articles got routed to the most capable model available. Technical documentation went through a specialized coding model for accuracy. The platform was using four different underlying AI models, but I only saw one interface.

The business implications are significant:

Companies are no longer locked into a single AI provider. If OpenAI raises prices or Claude releases a better model, platforms can switch behind the scenes. For end users like us, this means more reliability (if one model is down, requests route to alternatives) and better results (each task gets the best model for the job).

The vendors leading this trend? Anthropic’s Claude is particularly strong with multi-model architectures, and we’re seeing platforms build “model-agnostic” solutions that can plug in any AI backend. Even OpenAI is quietly supporting this trend by making GPT models easier to integrate alongside competitors.

One warning from experience: this flexibility comes with complexity. I’ve seen platforms where model switching created inconsistent outputs that confused users. The best implementations are transparent about which model is being used and why—something to look for when evaluating new tools.

Enterprise AI Adoption Accelerates (Finally)

For years, enterprise AI adoption was mostly pilots, proofs-of-concept, and “we’re exploring AI” statements in earnings calls. In 2025, that finally changed. I’m seeing real production deployments at scale, and the numbers back this up.

Here’s what shifted: compliance, security, and governance frameworks finally caught up. Two years ago, I had Fortune 500 clients who wanted to use AI but couldn’t get past their legal and security teams. Those conversations now take days instead of months, because there are established patterns, audit trails, and security certifications.

The enterprise AI software market is now the fastest-growing segment, projected to hit $50 billion by the end of 2025, according to recent IDC data. What’s driving this?

Real-world implementations I’m tracking:

A financial services client deployed AI for fraud detection across 40 million transactions monthly—something that was just a roadmap item in 2023. A healthcare system I consulted for is using AI for diagnostic assistance across 200+ physicians. A manufacturing company automated quality control inspection with computer vision AI, catching defects that human inspectors missed.

These aren’t flashy consumer applications. They’re boring, high-value, business-critical systems that generate measurable ROI. The average enterprise AI project I’m seeing now targets 20-40% efficiency gains in specific processes, with payback periods under 18 months.

What’s changed to make this possible:

- Better integration: APIs and connectors that actually work with legacy systems

- Clearer ROI models: We can now predict costs and benefits with reasonable accuracy

- Vendor maturity: Enterprise support, SLAs, and security certifications are standard

- Internal expertise: Companies have hired AI specialists who know how to implement this stuff

The flip side? Small and medium businesses are getting left behind. The AI tools and frameworks being built for enterprise customers often don’t scale down well. There’s a growing divide between companies with dedicated AI implementation teams and everyone else—something that concerns me as someone who works with businesses of all sizes.

The Rise of Domain-Specific AI Applications

Generic AI tools are still useful, but the real growth in 2025 is happening in specialized, industry-specific applications. Think less “AI writing assistant for everyone” and more “AI specifically trained on medical literature for oncologists” or “AI optimized for legal contract review in M&A transactions.”

I’ve tested dozens of these domain-specific tools this year, and the difference in quality is striking. A legal AI trained on millions of contracts understands nuances that a general-purpose AI completely misses. A radiology AI trained on medical images spots abnormalities with accuracy that approaches or exceeds human specialists.

Market sizing tells the story:

Healthcare AI is projected to reach $15+ billion in 2025, with applications ranging from diagnostic support to drug discovery. Legal AI is growing at 35% annually as law firms discover AI can handle document review, due diligence, and legal research more efficiently than junior associates. Financial services AI—covering everything from algorithmic trading to risk assessment—is approaching $20 billion globally.

Here’s what I’m advising clients: if there’s an AI tool specifically built for your industry, test it before settling for a general-purpose alternative. The specialized solutions are often 3-5x more expensive, but in my experience, they deliver 10x better results for domain-specific tasks.

Examples from my recent work:

- A medical practice switched from ChatGPT to a HIPAA-compliant medical AI and saw diagnostic suggestion accuracy improve from “occasionally helpful” to “consistently valuable”

- A law firm moved from general AI writing tools to legal-specific AI and cut contract review time by 60%

- An architecture firm adopted AI trained specifically on building codes and regulations, catching compliance issues that generic AI missed entirely

The challenge? These specialized tools require more training and onboarding. Your team needs to understand both the AI’s capabilities and the domain expertise to use them effectively. It’s not plug-and-play like consumer AI tools.

Agentic AI: From Assistants to Autonomous Systems

This is the trend that gets me most excited—and most nervous—about 2025. We’re shifting from AI as a tool you interact with to AI as an autonomous agent that takes actions on your behalf.

Let me explain what this looks like in practice. Traditional AI: you ask a question, it gives an answer, you decide what to do next. Agentic AI: you set a goal, and the AI figures out the steps needed, executes them, handles obstacles, and reports back when complete.

I recently set up an agentic AI system for a client’s customer service operation. Instead of AI just suggesting responses that humans review, it now handles the entire workflow: reads incoming tickets, classifies them, researches solutions in the knowledge base, drafts responses, checks if the response meets quality standards, sends it, and follows up if needed. Human oversight happens at the exception level, not at every step.

The market shift is dramatic:

Companies like AutoGPT, AgentGPT, and BabyAGI pioneered this space in 2023, but now major players are building agentic capabilities into their platforms. Salesforce AgentForce, Microsoft’s Copilot Studio, and Google’s Vertex AI Agent Builder all launched or significantly expanded in late 2024 and early 2025.

What’s making this possible:

- Better reasoning models: AI can now break down complex goals into subtasks more reliably

- Tool integration: APIs that let AI actually do things (send emails, update databases, schedule meetings)

- Improved safety: Guardrails and approval workflows that prevent AI from making catastrophic mistakes

- Lower costs: Running multi-step AI workflows is now economically viable for routine tasks

Here’s the honest truth: agentic AI is still early, and I’ve seen plenty of failures. An AI agent I tested for social media management once scheduled 47 posts in a single day because it misunderstood the goal. Another tried to book 12 meetings simultaneously because it couldn’t check calendar availability properly.

But when it works? The productivity gains are substantial. One client saw their marketing team go from managing 3 campaigns at a time to 10, with the same headcount. The AI agents handle routine execution while humans focus on strategy and creative direction.

What to watch for:

Companies are hiring “AI agent orchestrators”—people who design and manage fleets of AI agents. Job postings for these roles increased 400% in the first quarter of 2025, according to LinkedIn data. If you’re in operations, workflow automation, or process improvement, this skillset is worth developing.

The Open Source vs. Proprietary Battle Intensifies

One of the most fascinating dynamics in the AI software market right now is the tension between open-source and proprietary models. And in 2025, this isn’t just a technical debate—it’s reshaping competitive dynamics and pricing across the entire market.

Here’s the situation: open-source models like Meta’s Llama 3, Mistral, and others have gotten really good. I mean, legitimately competitive with proprietary options for many use cases. Last month, I ran a blind test with five marketing clients, comparing outputs from GPT-4, Claude, and a fine-tuned Llama 3 model. Three out of five couldn’t reliably tell which was which.

What this means for the market:

Pricing pressure is intense. When a company can self-host an open-source model for pennies per thousand tokens versus paying OpenAI or Anthropic $0.03-0.10, the economics start favoring open source—especially at scale. I’ve watched several enterprise clients calculate that switching to self-hosted open-source models would save them $200K+ annually.

But—and this is important—there are real tradeoffs. Open-source models require infrastructure expertise, ongoing maintenance, and responsibility for any outputs or issues. When a client asked me last week whether they should switch to open source, my answer was: “Can you hire two ML engineers to manage this, or are you better off paying the premium for a managed service?”

The market is bifurcating:

- Large enterprises with AI teams: Increasingly using open-source models for cost savings and data control

- Mid-market and small businesses: Sticking with proprietary solutions for simplicity and support

- Hybrid approaches: Using open-source for high-volume, low-stakes tasks and proprietary models for critical applications

The vendors feeling the most pressure? Those charging premium prices without clear differentiation. If your AI tool is just a wrapper around GPT-4 with a nice UI, customers are asking why they shouldn’t just use the API directly or switch to an open-source alternative.

One trend I’m watching closely: “open core” business models where the base AI model is open source, but enterprise features (security, compliance, fine-tuning tools) are proprietary. This seems to be finding a sweet spot between community adoption and sustainable revenue.

AI Development Tools: The Picks and Shovels Market

While everyone focuses on consumer-facing AI applications, some of the most interesting market growth is happening in AI development tools—the infrastructure that makes building AI applications easier.

Think of this as the “picks and shovels” of the AI gold rush. Companies like LangChain, Weights & Biases, Pinecone, and Hugging Face aren’t building end-user AI applications—they’re building the tools that other companies use to build AI applications. And this segment is absolutely exploding.

I’ve personally used at least a dozen different AI development platforms this year while building custom solutions for clients. The market has matured incredibly fast. Tools that were glitchy beta products in 2023 are now production-ready platforms handling billions of AI requests.

Key categories seeing growth:

Vector databases (Pinecone, Weaviate, Qdrant): Essential for AI applications that need to search through large amounts of data. The market is expected to grow 70%+ in 2025 as more companies build retrieval-augmented generation (RAG) systems.

LLM orchestration frameworks (LangChain, LlamaIndex, Semantic Kernel): These make it easier to chain together multiple AI calls, manage prompts, and build complex AI workflows. Adoption has increased 5x in the past 18 months based on GitHub activity.

AI observability and monitoring (Weights & Biases, Arize AI, WhyLabs): As companies move AI from experiments to production, they need tools to monitor performance, track costs, and catch problems. This was basically nonexistent two years ago; now it’s considered essential.

Prompt management platforms (PromptLayer, Humanloop, PromptBase): Managing and versioning prompts across an organization is harder than it sounds. These tools help teams collaborate on prompts, test variations, and ensure consistency.

What’s driving this growth:

Every company I work with is building custom AI applications now, not just using off-the-shelf tools. A marketing agency wants AI customized for their specific workflow. A healthcare provider needs AI that integrates with their EHR system. A logistics company requires AI optimized for their unique data.

Building these custom applications used to require deep ML expertise. These new development tools lower the barrier significantly—I’ve seen developers with no AI background ship functional AI features in weeks instead of months.

Investment trends:

Venture capital is pouring into this infrastructure layer. In Q1 2025 alone, AI infrastructure startups raised over $3 billion, according to Crunchbase data. Investors see this as more defensible than application-layer companies, which face intense competition and rapid commoditization.

If you’re a developer or working in tech, this is the area I’d recommend learning. The demand for people who can integrate AI into existing systems using these tools far outstrips supply. Every company I advise is hiring for this skillset.

Pricing Models Evolve: From Per-Token to Value-Based

Here’s a trend that directly impacts everyone’s budget: AI pricing is getting more sophisticated, and honestly, more confusing.

The per-token pricing model that dominated the early days is giving way to more creative approaches. I’m seeing subscription tiers, usage-based pricing, value-based pricing, and hybrid models—sometimes all from the same vendor depending on your company size.

What’s changed in 2025:

OpenAI, Anthropic, and Google have all introduced tiered pricing with volume discounts, reserved capacity options, and enterprise agreements. Last month, I negotiated a deal for a client that got them 40% off standard API pricing in exchange for a committed annual spend. These kinds of negotiations were impossible a year ago.

New pricing models I’m seeing:

- Outcome-based pricing: Pay based on results rather than usage. One AI customer service platform charges based on tickets successfully resolved, not API calls made.

- Seat-based with usage caps: Hybrid models where you pay per user but with included usage limits, then overage charges—similar to SaaS tools we’re familiar with.

- Tiered feature access: Basic AI capabilities included in standard pricing, advanced models cost extra. Microsoft 365 Copilot follows this pattern.

- Compute-hour pricing: For AI training and fine-tuning, paying for GPU/TPU hours rather than inference calls.

The challenge for buyers:

Comparing costs across vendors is nearly impossible now. I built a spreadsheet last month trying to calculate the true cost of five different AI platforms for a client’s use case. It took four hours and required assumptions about usage patterns, growth rates, and feature adoption.

My advice: forecast your AI usage as accurately as possible before committing to any pricing plan. Most vendors will let you test different tiers or negotiate based on projected volume. And watch out for overage charges—I’ve seen clients get surprise bills 3x their expected costs because they underestimated usage growth.

Where pricing is heading:

I expect continued downward pressure on per-token costs (inference is getting cheaper as models optimize) but increased premium pricing for specialized capabilities. The commodity AI features will trend toward free or near-free, while advanced features, customization, and enterprise support command higher prices.

Preparing for What’s Next: Practical Steps

After tracking these trends for months and working with dozens of clients navigating this market, here’s what I recommend you actually do with this information:

If you’re buying AI software:

Start with an audit of what you already have. Before buying another AI tool, check what’s included in your existing software licenses. You might discover your Microsoft, Google, or Adobe subscription already includes AI features you’re not using.

Test extensively before committing. The AI market is moving fast enough that a 90-day pilot will tell you more than any vendor pitch. Set clear success metrics and be willing to walk away if they’re not met.

Plan for a multi-vendor strategy. Don’t put all your eggs in one AI basket. The best implementations I’ve seen use 2-4 different AI providers for different use cases, with clear integration between them.

If you’re building AI products:

Differentiate through specialization or integration, not general capability. The days of “we’re building a better ChatGPT” are over unless you have extraordinary resources. Focus on solving specific problems exceptionally well or integrating AI into workflows in novel ways.

Build for the enterprise if you want sustainable revenue. Consumer AI is hit-driven and competitive. Enterprise AI is growing predictably with clearer monetization paths.

Consider open-source foundations with proprietary value-add. The hybrid model is proving sustainable—give away the core, charge for what enterprises actually need (security, compliance, support, customization).

If you’re investing in AI:

Infrastructure layer remains attractive. The picks-and-shovels approach is working—companies building tools for AI developers are seeing steadier growth than application-layer companies.

Watch for consolidation opportunities. Smaller AI vendors with good technology but weak distribution will increasingly become acquisition targets for larger platforms.

Enterprise solutions over consumer tools. The money in 2025 is following predictable, high-value B2B use cases rather than hoping for viral consumer adoption.

The Bottom Line: What 2025 Really Means for AI Software

Looking at where we are right now, the AI software market in 2025 isn’t about technological breakthroughs—it’s about practical implementation, market consolidation, and figuring out what actually delivers value.

The hype cycle is maturing. We’re past the “AI will change everything overnight” phase and into the “here’s what AI is genuinely good at” phase. That’s healthy, even if it’s less exciting for headlines.

The winners in this market are companies and individuals who focus on specific, high-value use cases rather than trying to be everything to everyone. Whether you’re buying, building, or investing in AI software, specialization and practical results are what matter now.

What surprised me most this year? How quickly the market went from “too many AI tools to choose from” to “most of the good stuff is consolidating into a handful of platforms.” That trend will likely accelerate in 2026.

My honest take after seven years in this space: We’re still early in the AI revolution, but we’re past the initial chaos. The foundations are being laid for AI to become as ubiquitous as cloud computing. Companies that treat this as a marathon rather than a sprint—investing in the right tools, building expertise gradually, and focusing on measurable outcomes—will be the ones still standing when the next wave of innovation hits.

The AI software market in 2025 isn’t about having the newest, shiniest tool. It’s about knowing which tools solve your specific problems, implementing them thoughtfully, and continuously adapting as the technology evolves. That’s been true for every major technology shift I’ve witnessed, and AI is no different.

What’s your biggest challenge with AI adoption right now? I’d love to hear what you’re seeing in your industry—the real trends often come from practitioners in the field, not analyst reports.